Establishing a corporation in Japan is an exciting milestone, but navigating Japanese tax regulations can often feel like learning a completely new language.

For many foreign founders, one of the most surprising regulations involves how you pay yourself.

Under Japanese Corporate Tax Law, director compensation is strictly monitored to prevent arbitrary profit manipulation.

Here are three essential points every foreign executive must understand about the “Regular Fixed-Amount Salary” (定期同額給与, Teiki Dogaku Kyuyo) rule to ensure their compensation remains tax-deductible.

Please note that the following rules apply to corporate directors and are not applicable to regular employees.

Strict Monthly Consistency

For a director’s remuneration to be recognized as a deductible corporate expense, it must qualify as a “Regular Fixed-Amount Salary.”

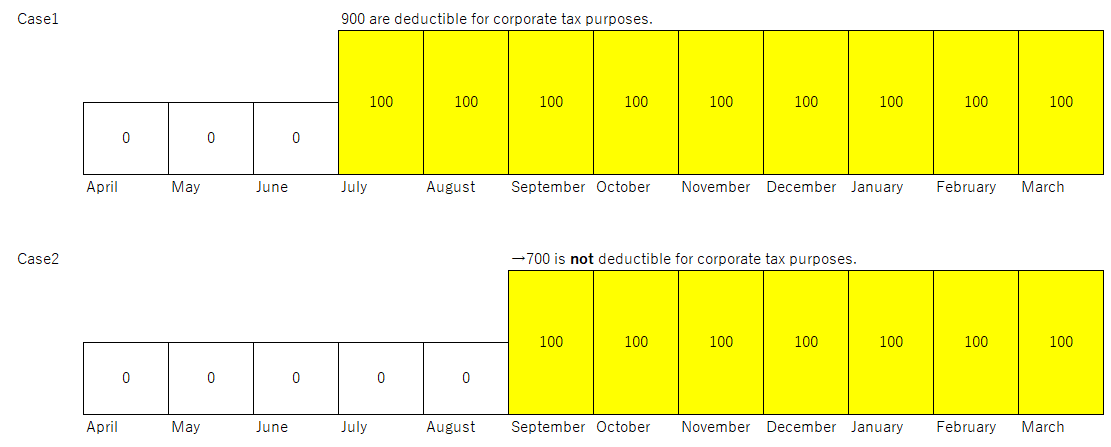

This means you must pay yourself the exact same gross amount every single month throughout the company’s fiscal year.

If your salary fluctuates—for example, taking ¥500,000 one month and ¥800,000 the next—the Japanese tax authorities will view this as an attempt to artificially reduce corporate taxable income.

Consequently, any amount exceeding the lowest monthly base will be denied as a deductible expense, resulting in a significantly higher corporate tax bill for your company.

When Can You Change Your Salary?

A common question from growing startups is: “What if the company does well and I want to give myself a raise?” You are absolutely allowed to increase (or decrease) your salary, but the timing is strictly regulated.

Under the Corporate Tax Law, you can generally only revise a director’s remuneration once per fiscal year. This revision must be officially resolved at the ordinary general meeting of shareholders (or by unanimous member consent in a Godo Kaisha) within three months from the start of your new fiscal year.

Once this new monthly amount is approved, it must remain locked in for the remainder of the year. Adjusting your compensation outside of this three-month window—whether a mid-year raise or a sudden pay cut—will typically render the changed portion non-deductible.

The only exceptions are extreme circumstances, such as a severe, unforeseen deterioration of the company’s financial standing.

For example, a company established in April would look like the diagram below.

The Pitfalls of Spontaneous Bonuses

Rewarding yourself with a year-end bonus after a highly profitable year is a standard global business practice. However, in Japan, spontaneous or profit-linked bonuses paid to directors are non-deductible.

If you wish to pay yourself a bonus and have it recognized as a deductible corporate expense, you must utilize the “Advance-Notice Director Bonus” system (事前確定届出給与, Jizen Kakutei Todokede Kyuyo). This requires you to determine the exact bonus amount and the exact payment date during the same three-month window at the beginning of your fiscal year. You must then submit a formal notification detailing this plan to the local tax office. If you deviate by even one yen, or pay the bonus even one day late, the entire bonus amount immediately loses its deductibility.

Summary

Planning your compensation in Japan requires foresight rather than flexibility.

By setting a realistic, fixed monthly salary at the start of your fiscal year and adhering to the strict deadlines for any adjustments or bonuses, you can protect your corporation from unexpected tax liabilities and ensure your business grows on a solid, compliant foundation.

Our Services

- Tax advisory services, spot tax consultations, support for starting individual businesses and company establishment, and support for startup financing, among others.

- We can handle taxes related to overseas transactions, international taxation, and English support.

- Service areas: Primarily in Nerima Ward, Shibuya Ward, Toshima Ward, Suginami Ward, Nakano Ward, Shinjuku Ward, and Setagaya Ward, as well as the 23 wards of Tokyo,

Nishitokyo City, Mitaka City, Musashino City, and other areas outside the 23 wards of Tokyo, including Kanagawa Prefecture, Saitama Prefecture, and Chiba Prefecture.

Nagano Prefecture (due to being my hometown).

*We can also provide nationwide support using online tools.”

- The content of the blog on this site is written based on various laws and regulations at the time of writing, so the information provided may not necessarily be the most up-to-date.

- The content is presented under limited conditions, and some specialized topics have been avoided to make the articles more accessible to the general public. While we strive to enhance accuracy, the blog administrators will not be held responsible for any damages or disadvantages that may arise from the use of the information provided in the blog (including information provided by third parties).

- When making decisions regarding your own tax issues, please make sure to consult with your tax advisor and make your own judgments at your own responsibility.